Wealth Tax Reality Check: It’s Unconstitutional

The Constitution’s apportionment clause makes wealth taxes clearly unconstitutional.

That’s not to say a wealth tax is impossible. Just as when federal income taxes were enacted, there is a way to have a legal wealth tax: the Constitutional Amendment process.

But to pass an Amendment, the Constitution first requires two thirds of the House and two thirds of the Senate. Then it requires 75% (i.e., 38 of 50) of the states to ratify. Even if it were to pass in both Congressional houses by 2/3rds, there are 61 state legislatures in Republican hands, and only 37 in Democratic hands. The odds of getting a new Constitutional Amendment to allow it are slim to none for the foreseeable future.

Why a Wealth Tax?

There’s perhaps no proposal more populist than taxing the owned property of the very wealthy. It regularly gets center-stage in stump speeches for the 2020 election. Two motivations are cited by wealth tax proponents: (1) Funds are needed for programs, and (2) America has a vast and growing wealth disparity.

Here’s Senator Warren, who frames it as a way to unite Americans (note, she means $50 million, not billion):

The 10-year plans put forward by Sen. Bernie Sanders cost about $97 trillion over ten years. For her part, Sen. Elizabeth Warren’s plans cost about $50 trillion over the same period. That’s a lot of money. How much? Just to calibrate it, you could zero out all US military spending — weapons, ships, salaries of all soldiers, supplies — and that’d pay for only about 10% of Sanders plans, and less than 20% of Warren’s plans.

A major pillar of the funding for each of these plans are new wealth taxes. This would be an entirely new federal idea — that tax on owned property would be owed every year. While real estate property taxes exist, they’re not done at a federal level; these are state and local county responsibilities, allowed by their State constitutions.

The proposed federal wealth taxes would start to kick in at $30 million of net worth for Sanders, and $50 million for Senator Warren.

Though the mechanics have yet to be spelled out, every year, presumably, wealthy households would have to assess their net worth, and pay an annual fee to the IRS.

On the surface, it’s a compelling notion, the idea that Jeff Bezos and Bill Gates, Wall Street Hedge Fund managers and the uber-wealthy should pay even more for the programs we want than they do today in income and other taxes. There’s no more attractive idea than that others pay for things. The majority of the dollars to be tapped is in wealth — i.e., property — not annual income.

“Why do I rob banks? Because that’s where the money is.”

Slick Willie Sutton, bank robber

The best estimates today are that such a wealth tax might raise between $2 and $4.3 trillion over ten years, meaning they’d fund between 2% and 8.6% of Sanders’ or Warren’s spending proposals. But these forecasts make a lot of highly debatable assumptions, such capital won’t flee, or that illiquid assets with subjective value like ownership in family businesses (or land or art) would be fairly valued, kept in the open and honestly reported.

Wealth tax proponents generally ignore the realities of what’s happened when large wealth taxes have been implemented in other nations. When wealth taxes are passed, the wealthiest flee or move assets elsewhere, resulting in far less revenue than originally forecast.

Capital has never been more global nor more mobile than it is today in the twenty first century. Billions of dollars can migrate at the click of a button.

Wealth Gap

The second rationale for such plans is to help narrow the vast and growing disparity between the nation’s wealthiest and poorest households.

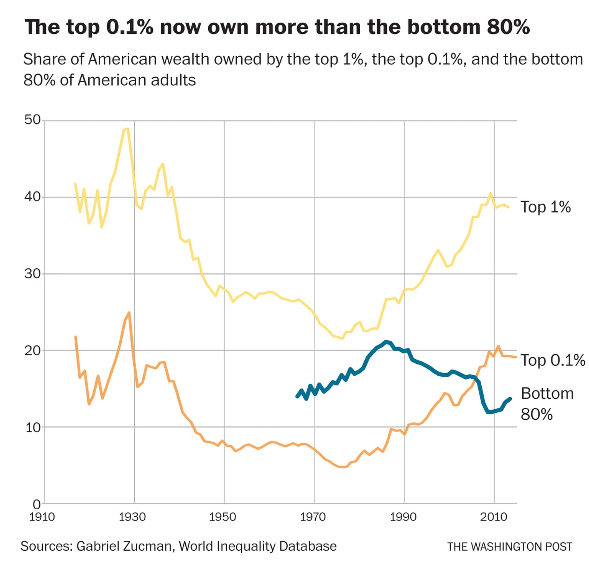

As this chart illustrates, the Top 1% of households as measured by net worth now own more than the bottom 80%, and that this separation has been increasing since the late 1980’s, which began a period of both innovation — the Information Age, which helped create spectacular wealth for a relatively few pioneers, and financial deregulation.

This wealth gap is mostly explained by appreciation of owned assets: stocks, bonds, land, and more. Roughly 55% of adult Americans own stock, 45% do not.

So the motivation for such a tax is twofold.

But there are big problems. Some have cited that it’ll raise far less than they plan. Others focus on capital flight. Still others say it’ll depress charitable contributions.

But first and foremost, such a wealth tax is clearly unconstitutional.

The Constitution is a Power Limiting Document

Let’s first begin with the uncomfortable reality for the leftward side of the Democratic Party. The United States Constitution is a document which fundamentally limits what the federal government can do. That means, adding new powers to centralize control and tax from Washington DC is a very hard thing to do, given the clear words in the Constitution.

Specifically, The Tenth Amendment to the United States Constitution, introduced by James Madison, limits the power of the federal government:

The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.

Tenth Amendment of the United States Constitution

Read that again. It’s text that too few people know. It means that unless The Constitution explicitly enumerates the power, it is assumed that the States or the people have that power, and the federal government does not. Neither a President nor Congress can claim powers that aren’t already allowed by the Constitution.

The Tenth Amendment originated from the framers’ fear, particularly that of James Madison, that the federal government would eventually have too much power over the lives of individuals and of the States. By adding and adopting this amendment, the framers made it clear that they expect federal powers to be limited.

And the power to levy a tax on property (wealth) is not explicitly granted to the federal government. The federal government does have power to enact a “Direct Tax”, but only if it is “Apportioned to the States by population.”

The Apportionment Clause

In Article I, Section 3, The United States Constitution makes it crystal clear that Direct Taxes must be Apportioned to the States by Population:

Representatives and direct Taxes shall be apportioned among the several States which may be included within this Union, according to their respective Numbers

Article I, Section 3 of the US Constitution

You may ask: why then, are federal income taxes legal? Good question: the answer is because we’ve been through such a moment in our history before, and an Amendment was enacted.

We didn’t originally have federal income taxes when the Constitution was written.

The history of federal income taxation in the United States began in the 19th century, with the imposition of income taxes to fund war efforts. Proponents quickly found that the practicalities of ensuring that an income tax was “apportioned among the States” would make the new income tax run afoul of the Constitution’s apportionment clause, and sure to be overturned by the Supreme Court of the United States. This valid concern came from the fluid nature of changing populations, and the prospects of new states joining the Union.

So, in order to make federal income taxes legal, Congress put forward the Sixteenth Amendment in 1909 to “get around” this provision.

But here’s the thing. The Sixteenth Amendment narrowly restricts the override to income, not wealth, nor property taxes:

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

Sixteenth Amendment, US Constitution

In other words, the Constitution still very much requires that all Direct Taxes be apportioned by State. And a wealth tax is very much a Direct Tax, meaning directly laid upon individual citizens (and households), not States. In fact, the Supreme Court has specifically ruled that a tax on one’s land is a Direct Tax.

Yes, real estate property taxes are legal — but those are imposed by counties (or Cities or States.) They’re not levied by the United States federal government. You don’t write a check to the IRS for your property tax.

So what does this Apportionment Clause mean in practice? Basically, it requires that Congress follow a specific process. First, it must determine what revenue it wants to raise, then apportion that revenue by State (based on population), then craft such a tax to get it.

Given the mobility of residence of the households subject to such a hypothetical tax, that is impractical and not a means by which wealth taxes could be created.

The practical reality is that the wealth tax as contemplated by Sanders and Warren would affect some 75,000 households. But those 75,000 households are very much not distributed evenly among the States, and certainly not by population. For instance, Nebraska, a relatively low-population state, has billionaire investor Warren Buffett. Here in Washington State, we’ve got several billionaires claiming residence, including Bill Gates, Jeff Bezos, and Steve Ballmer.

The federal government does not have Constitutional power to lay a net direct tax on individuals without it being so apportioned.

How to Amend The Constitution

Luckily for wealth tax supporters, the framers created a vehicle to modify the Constitution: the Amendment Process.

To amend the constitution, there are three basic methods. Each are difficult and time-consuming processes. That’s a feature, not a bug. Since the states ratified the original Constitution in 1788, only 27 out of 11,000 proposed amendments have ever been adopted.

- Article 5 of the Constitution governs how amendments are made. They can be proposed either by Congress or by a “constitutional convention.” The latter method, however, has never been used. All current amendments to the U.S. Constitution have been proposed by the U.S. Congress and not by constitutional convention.

- When Congress proposes an amendment, they do so in the form of a joint resolution agreed upon by a two-thirds majority in both the House of Representatives and the Senate.

- From there, the amendment goes to the National Archives and Records Administration, which packages and ship it to the states for approval. Three-fourths of state legislatures or conventions (that is, 38 out of 50) must approve the motion for the amendment to pass.

- For an amendment to be proposed via a constitutional convention, two-thirds of the state legislatures must call for it. That convention proposes the amendment which is then sent to the states to be approved, and approval must be granted by three-fourths of the legislatures or conventions among the states

Take note of Steps 2 and 3 above: it must first pass 2/3rds of both houses, and perhaps even more critically, be ratified by three-fourths of the States. That’s 38 of 50 States.

But at current writing, 61 state legislative chambers are held by Republicans and 37 are held by Democrats. So a Constitutional Amendment is quite unlikely for the foreseeable future.

Warren on Wealth Tax

Warren’s plan places a 2% levy on fortunes above $50 million in net worth. She “sells” this, rather disingenuously in my view, as a “two cent tax.” That’s because it’s not actually two cents, it’s two cents on every single dollar you own (liquid or not), above $50 million in wealth. This owned wealth, by the way, has already been taxed.

Her plan also places a 6% levy on fortunes above $1 billion in net worth.

See her campaign website.

Sanders on Wealth Tax

Sanders starts taxing wealth of $32 million in net worth at 1% per year, which increases to an 8% tax on fortunes above $10 billion.

See his campaign website.

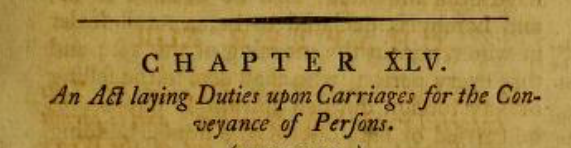

History: Carriage Tax in 1794

The idea of taxing wealth isn’t a new one. In fact it predates even a federal income tax.

The story begins in 1790’s, and George Washington wanted to raise money for the federal government. He and Alexander Hamilton thought that taxing the wealthy was a very good idea.

What’s a good way in 1794 to determine who’s wealthy? Carriages.

So Hamilton and Washington and their staffs wrote An ACT laying duties upon Carriages for the Conveyance of Persons.

Just like Warren’s wealth tax proposal, it was progressive, hitting the more expensive carriages harder.

This Act set off a huge debate within the country about what kind of taxing power the founders wanted the federal government to have.

The Jeffersonian Republicans strongly opposed the taxes at the time. In particular, James Madison, one of the main architects of the Constitution found it improper. He indicated that the Carriage Tax ran afoul of the apportionment clause, and brought it to the Supreme Court in 1796.

Alexander Hamilton himself argued at the Supreme Court on behalf of the Carriage Tax. He argued for three hours. The Supreme Court found in favor of the Carriage Tax, feeling that the apportionment clause was only reasonably interpreted to apply to land and slaves. The history of the clause, they argue, comes from the Constitutional framers wanting to assure Southern slave states that a tax on property and slaves would never be enacted.

The basis of the Supreme Court decision was that a carriage tax was not a “direct tax.” This all sounds like great news for wealth tax proponents, but there’s a huge catch: the Court very specifically noted in that decision that a tax on land would be a direct tax.

By the time the Jefferson administration came to office, the Carriage Act was repealed. (A victory for Big Carriage.)

And a later decision (Pollack v. Farmers’ Loan and Trust Co.), the Supreme Court noted “We are of the opinion that taxes on personal property, or on the income of personal property, are likewise direct taxes.“

By 1913 the Sixteenth Amendment was adopted. And in the 1916 case of Brushaber v. Union Pacific Railroad Co., Chief Justice White explained that the “[Sixteenth] Amendment contains nothing repudiating or challenging the ruling in the Pollock Case that the word ‘direct’ had a broader significance, since it embraced also taxes levied directly on personal property because of its ownership, and therefore the Amendment at least impliedly makes such wider significance a part of the Constitution….”

So today, it’s very hard to make the Constitutional argument that a tax on total wealth is not a direct tax by the federal government, as there are several times that the Supreme Court has gone on record to confirm it.

One interesting thought experiment — would this mean that if America ultimately embraces a wealth tax, might it first take the form of a tax on net wealth exempting land to avoid some of these very Supreme Court issues? Perhaps. In that case, you could see literally billions, perhaps trillions of dollars in holdings migrate to the purchase of land. (And is it land in the United States only, or land anywhere?)

More reading: The Unconstitutional Tax on “Unrealized Capital Gains” | AIER, Phil W. Magness

Video Commentary

A couple of quick video overviews that I found helpful for context are below.

CNBC Discussion

Two Lawyers Argue: Yes it is, No it isn’t.

To be sure, lawyers can be found who argue that a wealth tax is Constitutional, as well as lawyers who argue that it is clearly not Constitutional without an Amendment.

For those who wish to go much deeper, the best polemic I was able to find that argues in favor of the constitutionality of wealth taxes is a piece by Law Professor Calvin H Johnson. He and Erik M. Jensen (emeritus) argue back and forth in the ABA journal, bringing in case law and analogous circumstances.

I’ve shared the links below.

In terms of practical reality, however, such a debate means that such a wealth tax would be fairly immediately challenged, right up to the Supreme Court. And I’d ask you to consider the odds that the existing federal court circuits and especially today’s Supreme Court of The United States would find wealth taxes either (a) not a “direct tax” or (b) otherwise Constitutional. Given that there’s now a 5-4* conservative bent on the court, I think the odds are very slim. [*EDIT: This post was written before Amy Coney Barrett was appointed, taking Ruth Bader Ginsberg’s seat — which way do you think she’ll vote?]

A Wealth Tax is Constitutional, Calvin H Johnson, John T. Kipp Chair in Corporate and Business Law, University of Texas

Rebuttal: “An Unapportioned Wealth Tax Has Constitutional Problems“, Erik M. Jensen, Coleman P. Burke Professor Emeritus of Law, Case Western Reserve University, Cleveland, OH

Sur-Rebuttal: “A Sur-Rebuttal to Professor Jensen on the Constitutionality of an Unapportioned Wealth Tax“, Calvin H Johnson, John T. Kipp Chair in Corporate and Business Law, University of Texas

Conclusion

It’s important that supporters of the wealth tax idea understand that it would be quickly challenged as unconstitutional, and today’s Supreme Court is almost certain to agree. Thus, supporters need to have a realistic sense of how to enact a Constitutional Amendment to allow it, and/or factor the likelihood of this into their assumptions about ways to raise revenues for the plans they’d like to see.

Reading

[1] Is a Wealth Tax Constitutional?, NPR’s Planet Money Podcast

[2] Here’s Why Elizabeth Warren’s Wealth Tax is Completely Unconstitutional, The Federalist, August 8 2019

[3] Elizabeth Warren’s Wealth Tax is Unconstitutional, National Review, January 24 2019